Economic turbulence is further entangling the complex financing process for developers and investors.

Source: “How Affordable Housing Developers Solve the Funding Puzzle” by Gail Kalinoski for Multi-Housing News on June 27, 2023

Economic turbulence is further entangling the complex financing process for developers and investors.

Financing affordable housing developments has long been like assembling a jigsaw puzzle, but industry experts say the past year’s economic headwinds, including higher interest rates, rising costs and bank failures, have made putting deals together even more challenging. The result? It’s taking more funding sources to get deals, especially those using Low-Income Housing Tax credits, to pencil.

“It has been increasingly rare for an affordable housing development to get to the closing table without any kind of soft debt, seller financing, GP advance or tax abatement in this high interest rate environment,” said Julie Sharp, executive vice president, Tax Credit Equity at Merchants Capital. “Furthermore, pricing has been impacted by some bank failures. We’ve seen some pullback among regional banks in the equity space.”

“It’s been a double hit to project developers because you have higher interest rates and you also have lower tax credit equity pricing.”

Although some deals are getting tougher to underwrite, states are offering tax abatement and other soft sources, including American Rescue Plan funds to close gaps, Sharp said.

Derek Hammond, CFO of affordable housing at Flaherty & Collins Properties, which often uses either 9 percent or 4 percent LIHTC in its projects, said he is not seeing any deals close right now with only federal LIHTC. To fill the funding gaps, sponsors are relying on state and local resources.

In January, Indianapolis-based F&C announced four development projects to create or upgrade affordable residences in Indiana and Missouri. They financed each of the projects, which total $80 million, with numerous funding sources.

In Kansas City, Mo., for example, F&C, in partnership with Twelfth Street Heritage Development Corp., is rehabbing Jazz Hill, a 197-unit affordable housing community spread among 11 buildings for $35 million. Financing includes $11.3 million in federal LIHTC; $4.2 million in federal historic tax credits; $2.4 million in state historic tax credits; $9 million in permanent debt; $6.6 million in soft funds, including $4.1 million in Kansas City Central City Economic Development funds; a $1.5 million deferred developer fee; and a tax abatement.

It’s a similar scenario for other developers.

“I would say, right now, all our deals are using LIHTC, either 4 percent or 9 percent, and a mix of state and local financing, with obviously the LIHTC folks, the private equity and private lending along with it,” said Welton Jordan, chief real estate development director at nonprofit affordable housing developer EAH Housing, which operates in California and Hawaii. “That’s the sauce to get affordable housing built today.”

LIHTC to the rescue

There is hope LIHTC will be expanded through the bipartisan Affordable Housing Credit Improvement Act currently before Congress. While bills have previously been proposed, these bills have strong bipartisan backing on the Hill, according to J.P. Delmore, assistant vice president for government affairs at the National Association of Home Builders.

On May 31, The ACTION Campaign, a national coalition of 2,400 national, state and local organizations and businesses, sent a letter to Congress supporting the legislation. If passed, the changes are estimated to produce nearly 2 million more affordable housing units over 10 years, according to Novogradac.

Key provisions include increasing 9 percent credit allocations, generally reserved for new construction, by 50 percent and lowering the threshold of private-activity bond financing from 50 percent to 25 percent to enable more 4 percent bond deals.

“More projects will get funded,” Delmore said. “The demand is there.”

The 4 percent change is likely to have an immediate impact. “You could almost double the amount of deals that could be awarded bonds, and ultimately credits, and be funded almost immediately,” he said.

Corine Sheridan, senior vice president & head of acquisitions with Berkadia Affordable Housing, agreed, noting when applications go into the state housing agencies for credit, the LIHTC are oversubscribed three to four times the amount that’s available.

If passed, states might be able to increase the maximum amount of 9 percent credits developers are allowed to apply for each project, thereby decreasing the need for other soft sources and permanent debt, Sheridan said.

“This would enable states and localities to spread their funding resources to creating or preserving additional housing units,” she noted.

Flaherty & Collins Properties is renovating Emerald Pointe, a 168-unit affordable housing community in South Bend, Ind., as part of an $18.4 million rehabilitation project funded by several sources including $6.3 million in LIHTC equity, a $10.6 million permanent loan, a $950,000 seller note and a payment in lieu of taxes. Image courtesy of Flaherty & Collins Properties

GSEs see growth

Sheridan, who implements and manages the tax credit syndication team’s acquisition strategy, said Berkadia expects fairly significant growth in 2023 as they build up 2022, during which they added several new developer partners on the LIHTC side and a new tax credit investor: Freddie Mac Multifamily.

The GSE created a LIHTC syndicator fund with Berkadia Affordable Tax Credit Solutions in September, aiding the agency’s effort to invest up to $850 million in equity annually to develop and preserve affordable housing.

Freddie Mac scaled its LIHTC program up after the Federal Housing Finance Agency raised the annual LIHTC equity investment cap for Freddie Mac and Fannie Mae from $500 million to $850 million in 2021. [They] rolled an unused balance of $175 million in 2021 to 2022, further increasing its capacity for LIHTC equity investments last year and had a record nearly $1 billion in LIHTC equity investments, up from $675 million in 2021. Freddie Mac also has carryover this year, which has pushed its capacity to above $850 million.

Berkadia, Sheridan said, closed its first bond deal with Freddie Mac in December. Most of the LIHTC transactions with Freddie Mac so far have been 4 percent LIHTC deals, but she noted their transactions will encompass both 4 percent and 9 percent developments.

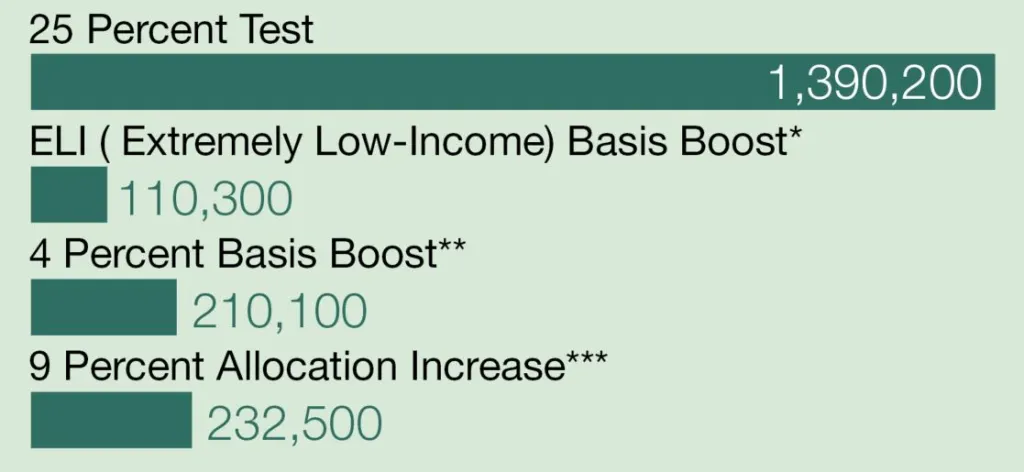

Proposed Increase in Affordable Rental Homes Financed by AHCIA Provisions

*Estimate includes units financed by 9 percent and 4 percent LIHTCs.

** The 4 percent basis boost includes: a discretionary 30 percent boost for private activity bond-financed properties; a 30 percent boost for properties in rural areas; and a 30 percent boost for properties in Native American areas.

***The 12.5 percent increase in 9 percent LIHTCs that expired at the end of 2021 is assumed to be reinstated in 2023 and made permanent. This estimate excludes the 9 percent LIHTC units financed by the ELI basis boost.

Source: Novogradac

Fannie Mae said in a prepared statement that its LIHTC investments provide a reliable source of capital and serve as a stabilizing influence on the affordable housing market. During 2021 and 2022, Fannie Mae committed all of its $1.7 billion cap in LIHTC investments, which created or preserved more than 35,000 affordable units. Since re-entering the market five years ago, Fannie Mae has provided more than $3 billion in equity investments. The GSE stated its Multifamily Affordable Housing volumes totaled more than $10.3 billion in 2022, up nearly 7 percent from $9.6 billion in 2021.

Last year, Freddie Mac exceeded its affordable housing goals. This year, the first quarter has started off slow with $6 billion of new activity, down 60 percent year-over-year. Freddie Mac noted all market volume is down, but they do typically see an uptick in business during the second half of the year. They expect that to be the case this year as well and are actively seeking to hit all their goals.

Peter Lillestolen, senior director of production for Freddie Mac Multifamily, said the GSE recently rolled out broader financing options under the Targeted Affordable Housing Bridge Loan program.

“We’re providing more flexibility with the new offerings, which includes non-LIHTC properties that have a long-term affordability commitment, and not just tax credit properties,” Lillestolen said. “These short-term bridge loans allow borrowers to quickly acquire a property and adequately address the scope of work and source of funds they need to rehab.”

Freddie Mac also recently launched a Workforce Housing Preservation program aimed at borrowers providing a private-sector approach to help solve the affordable housing crisis through voluntary rent restrictions, Lillestolen said. In return for setting aside units at affordable levels, Freddie Mac offers competitive pricing and credit terms.

Fannie Mae and Freddie Mac are “leaning into” affordable deals to meet their regulatory mission mandates, said Sarah Garland, affordable housing debt & structured finance leader at CBRE.

“When I say they’re leaning in, they’re doing things I don’t think I’ve ever seen them do before,” Garland said. “They’re doing extended amortization. They’ll have conversations about debt service and interest only.”

The agencies are also doing forward commitments on non-LIHTC deals to encourage more workforce housing construction or substantial rehabs, Garland noted, where previously they were reserved for LIHTC transactions.

Flaherty & Collins Properties is rehabbing Jazz Hill, an affordable community in Kansas City, Mo., for $35 million. The financing includes $11.3 million in federal LIHTCs, $4.2 million in federal historic tax credits, $2.4 million in state historic tax credits, $9 million in permanent debt and funds from additional sources. Image courtesy of Flaherty & Collins Properties

HUD deals

At Merchants Capital, the firm’s affordable debt production in 2022 was $5.9 billion, a 90 percent increase from $3.1 billion in 2021. Part of that growth came from an increase in Freddie Mac Targeted Affordable production and HUD 221 (d)(4) deals.

In the past six months, HUD has been increasingly competitive with its 221(d)(4) product, which insures mortgage loans to build new construction or substantially rehabilitate multifamily rental or cooperative housing, offering high-leverage, nonrecourse, fixed-rate loans with terms up to 40 years, said Scott Thurman, head of FHA lending at CBRE. It’s often paired with LIHTC and private-activity bonds.

“You can get increased leverage depending on the level of affordability, and you get lower debt coverage,” he said.

Olive Tree Holdings and its affiliate Olive Tree Affordable Housing are using a HUD-insured mortgage to complete $7.8 million in capital improvements at The Life at Westpark, a 312-unit affordable housing development in Houston. Olive Tree Affordable Housing, which has used LIHTC to rehabilitate and preserve more than 4,400 affordable housing properties, has extended Westpark’s affordability status for more than seven decades.

“HUD is a phenomenal long-term option in the current environment,” said Vice President Kevin Marshall-Moran. “Really in any environment they’re going to likely be the best priced alternative in the market.”

Olive Tree, Marshall-Moran said, also partners with mission-driven investors that have impact funds and affordable housing preservation capital, such as American South Fund Management, a joint venture between SDS Capital Group and Vintage Realty Co., which earlier this year provided funding for Olive Tree to make capital improvements at a newly acquired 429-unit affordable community in Wilmington, N.C. It was their fifth partnership.

State legislative changes

More than 20 states and Washington, D.C., have state tax credit programs, like LIHTC, to help finance affordable housing, and others, like Ohio, are considering them this year. Florida recently approved the Live Local Act, which is the largest investment in housing in the state’s history, appropriating $711 million for affordable and workforce housing this year–nearly double 2021’s investment. It also incentivizes housing development through tools that include raising tax credit limits, offering property tax abatements, easing zoning regulations, and banning rent control.

“There’s no place where there’s been more migration and more need for affordable housing than Florida,” said Aaron Pechota, executive vice president of development at The NRP Group in Cleveland, a multifamily developer and manager of affordable and market-rate housing. “I’d love to see other states take an aggressive approach like that.”

Amanda White, government affairs director for the Florida Apartment Association, said the land development provisions “are already opening doors across the state with new housing opportunities.”